News

Stay up to date on the latest crypto trends with our expert, in-depth coverage.

NVDA may be a clue

TradingView·2026/05/06 22:45

White House targets July 4 for key crypto law approval

Cointurk·2026/05/06 22:39

With Bitcoin on a Steady Uptrend, What Can We Expect Next? Will the Journey to $100,000 Continue?

CryptoNewsNet·2026/05/06 22:36

Bullish Signal? Crypto Funds Log 5th Consecutive Week Of Inflows

Newsbtc·2026/05/06 22:36

Fed's Goolsbee: US‑Iran conflict is an inflationary shock

FXStreet·2026/05/06 22:33

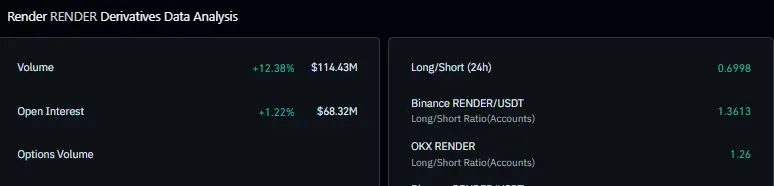

Render Price Rally Extends as AI Compute Demand Fuels Momentum: Is $5 Back in Play?

Coinpedia·2026/05/06 22:30

‘XRP Has Clarity’: Brad Garlinghouse Says He Has Chosen To Ignore Hoskinson’s ‘Stuff’

Coinpedia·2026/05/06 22:30

Bitcoin Near $83,000 While Oil Crashes 12% below $90 – Cryptoquant eyeing $93K

Coinpedia·2026/05/06 22:30

Clarity Act All New Updates: Moreno Says Bill Could Be Signed Before July 4 as Odds Hit 67%

Coinpedia·2026/05/06 22:30

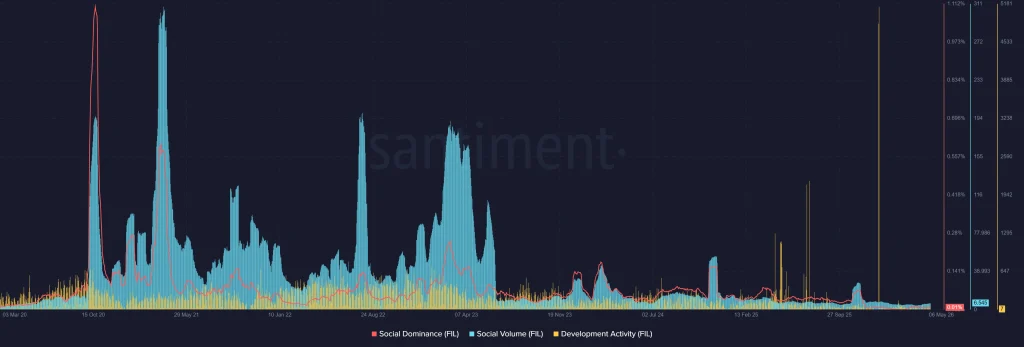

Can Filecoin Price (FIL) Recover From 99% Fall Or Is It Now a Dead Crypto Asset?

Coinpedia·2026/05/06 22:30

Flash

06:50

SecondFi: A small number of Cardano wallets were affected by security issues; the platform has entered maintenance modeForesight News reported that the self-custody financial platform SecondFi posted on Twitter that it has discovered a security issue affecting a small number of Cardano wallets. The issue is now under control and the affected functions have been suspended. To protect users, SecondFi has temporarily entered maintenance mode, all frontend interactions are paused, and users are currently unable to trade. The team is working hard to restore platform functionality.

06:44

Silver falls below $64 to a three-month low; bears dominate as the market focuses on the key $61 supportSilver drops below $64, hitting a three-month low; bears dominate the market with attention on the key $61 support level

06:43

A certain whale has closed 500,000 CL long positions, with a total loss exceeding $2.94 million.According to Odaily, a whale has completely closed 500,000 CL long positions, with a total loss exceeding 2.94 million US dollars.