News

Stay up to date on the latest crypto trends with our expert, in-depth coverage.

VeChain (VET) Price Prediction 2026, 2027 – 2030: Long-Term Forecast and Market Outlook

Coinpedia·2026/02/04 05:30

Are We in a Bear Market for Bitcoin? Anthony Pompliano Responds

BitcoinSistemi·2026/02/04 05:03

Amazon Q4 Earnings Preview: AWS Momentum + AI Investments = Another Explosive Beat?

Bitget·2026/02/04 04:58

Ripple Custody Powers $280M Diamond Tokenization on XRP Ledger

Cryptotale·2026/02/04 04:54

The Commodities Feed: Oil prices climb amid renewed US-Iran tensions

101 finance·2026/02/04 04:30

Bitcoin $40K Doom Incoming? Monero and Litecoin Lose Momentum, While APEMARS Sparks as the Best Altcoin Investment – Top 1000x Crypto Presale

BlockchainReporter·2026/02/04 04:15

Bitcoin Whale’s Stunning $118M Loss: Analyzing the Strategic Sell-Off of 5,076 BTC

Bitcoinworld·2026/02/04 04:06

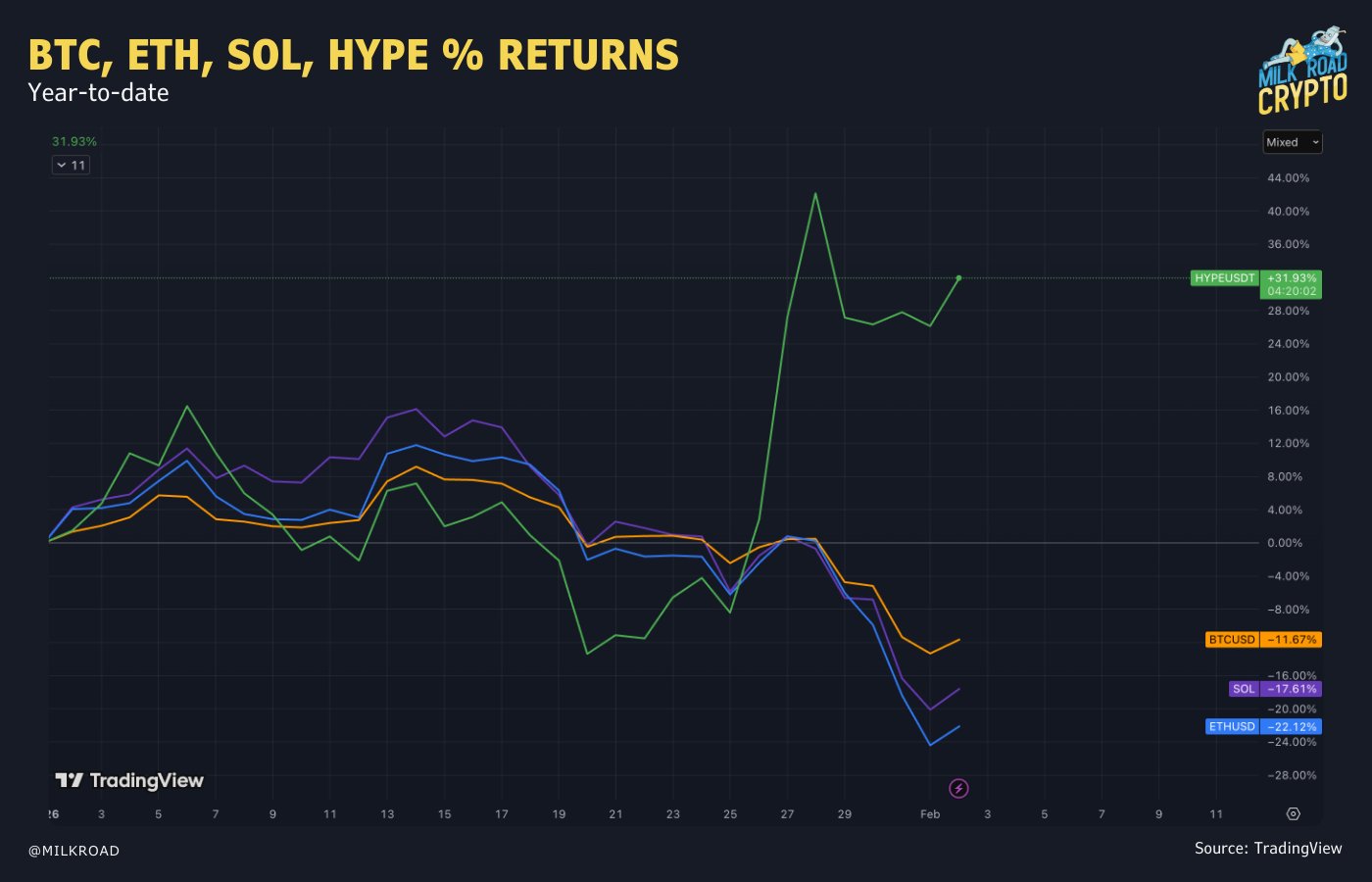

Hyperliquid: THIS is why HYPE is breaking out in a falling crypto market

AMBCrypto·2026/02/04 04:03

US Dollar remains stable, yen fluctuates as Japan election approaches

101 finance·2026/02/04 03:30

Flash

01:19

Cryptocurrency holdings and returns for U.S. President Trump and JD VanceUS President Trump has earned a profit of 2.3 billion dollars from the crypto industry, including 500 million dollars with WLFI and 635 million dollars with TRUMP. The media company's legal settlement brought in 80 million dollars. Currently, he holds more than 100 million dollars in BTC and ETH. Vice President JD Vance holds 500 thousand dollars in BTC. (Ai Yi)

01:18

CATL resumes production capacity of 100,000 tons of lithium carbonate```htmlGolden Ten Data reported on July 1 that a major development has stirred the lithium battery industry chain. According to market sources, Contemporary Amperex Technology Co., Ltd. was approved for the safe production permit of the Jianxiawo lithium mine on June 29. On June 30, media confirmed this news through authoritative channels, and further learned that the Jianxiawo lithium mine officially resumed production on the evening of June 29. Industry insiders stated: "The annual production capacity of lithium carbonate at Jianxiawo lithium mine is about 100 thousand tons, and this resumption will have a positive effect on the stable supply of upstream raw materials for the lithium battery industry chain."```

01:16

Spot gold fell nearly $20 in the short term, hitting a new intraday low at $3,979.09 per ounce, down about 0.7%. The decline was driven by persistently high expectations of Federal Reserve rate hikes and a rebound in the US dollar index, which is currently up 0.13% to around 101.30.Spot gold fell nearly $20 in the short term, hitting a new intraday low of $3,979.09 per ounce, a decline of about 0.7%. This is due to persistent expectations of Federal Reserve interest rate hikes and a rebound in the US Dollar Index. The US Dollar Index is currently up 0.13% to around 101.30.

News